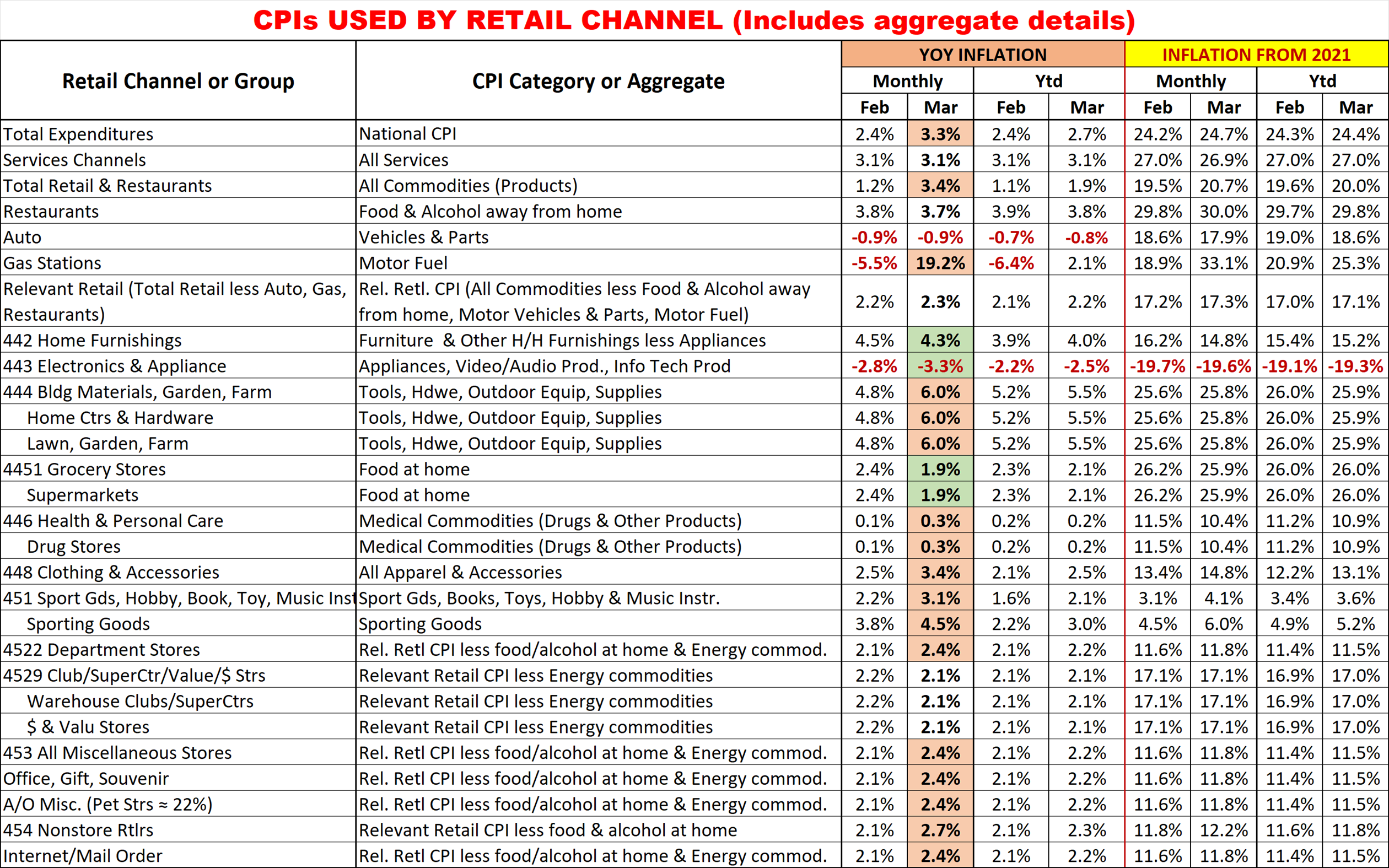

2024 Veterinary Spending was $41.26B – Where did it come from…?

Now we will turn to Veterinary Services. For years, Veterinary Services have had high inflation. This has resulted in CU income becoming the dominant factor in spending and a reduction in visit frequency.

In 2017 low inflation drove a 7.2% increase in visit frequency and a $2.5B spending lift. In 2018 inflation returned to normal. Consumers spent $0.56B more (+2.7%), but inflation was 2.6% so almost all of the lift was from higher prices. In 2019 the situation got worse. Consumers spent $0.58B (+2.7%) more but inflation was 4.1% so there was a decrease in the amount Vet Services purchased. In 2020 the pandemic hit, and Pet Parents focused on needs – Food & Veterinary. Veterinary spending grew $3.05B, (+14.0%). In 2021, this behavior grew even stronger and produced a record $7.82B (+31.5%) increase. In 2022 inflation reached 8.8%. Spending fell -$2.95B (-9.0%) but the amount of Vet Services sold fell 16.4%. In 2023 inflation was 9.4% but Vet Care is needed so spending grew $5.95B (+20.0%) – with inflation, +9.7%. In 2024, inflation slowed to 7.4% and the lift was still $5.60B, +15.7%. With inflation, it was really +7.7%.

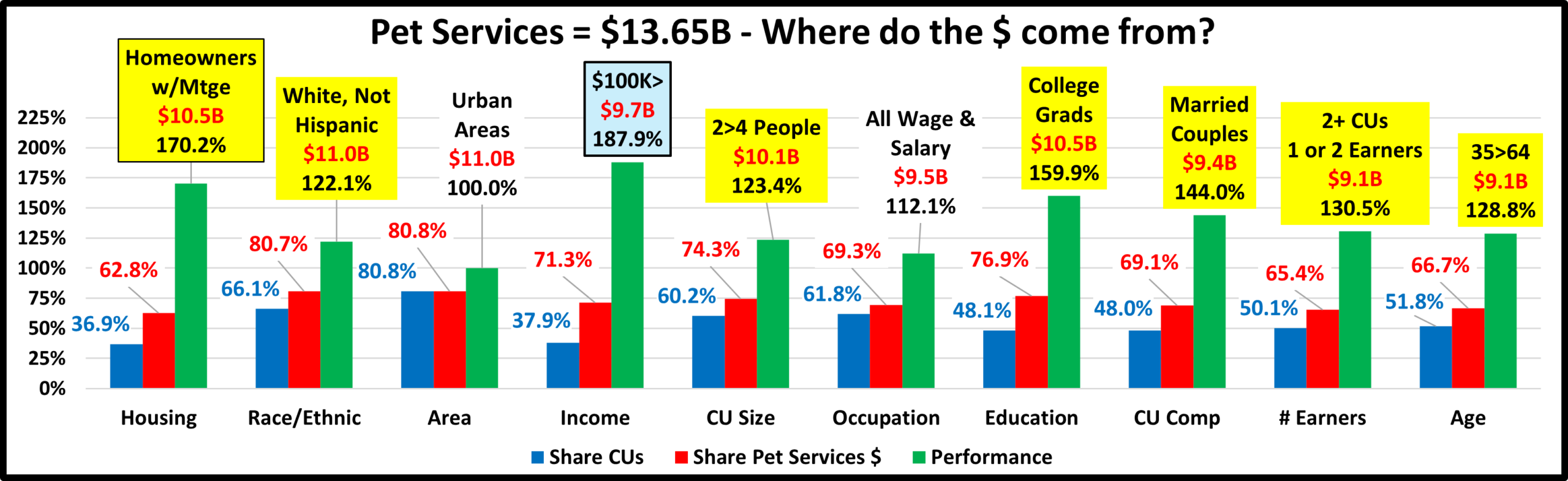

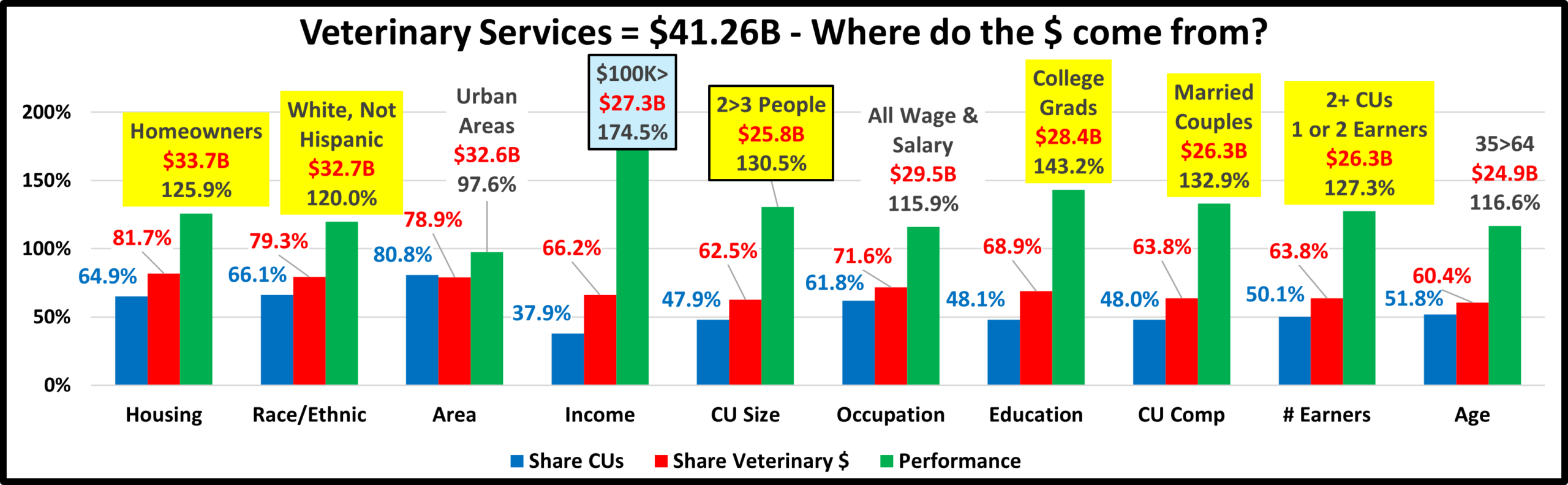

We’ll start with the groups who were responsible for most of Vet spending in 2024 and the $5.6B increase. The 1st chart details the biggest Vet spenders for 10 demographic categories. It shows share of CU’s, share of Vet spending and their performance (Share of spending/share of CU’s). In performance – 7 groups perform at 120+%, 2 more than 2023 & 1 more than 2018>2021. This is also 1 more than Supplies, 2 more than Food, but 1 less than Services. These big spenders are performing well but it also signals that there is still disparity between the best and worst performing demographics in this “needed” segment. Only the CU Size & Income groups are different from Total Pet and the categories are listed in the order that reflects their share of Total Pet $pending. Again, High Income is the most important factor in Spending.

- Housing – Homeowners (81.7%) up from 81.2% Homeownership is a major factor in pet ownership and spending in all industry segments. In terms of importance to Veterinary spending, their 125.9% performance rating is up from 124.8%, but they dropped to 6th from 5th place in importance. Only Homeowners w/o Mtge spent less. Renters were +12.5% while All Homeowners were +16.5%. This produced the small gains in share & performance for Homeowners. We should also note that Homeownership is definitely not as important to Veterinary Spending as it once was. In 2015 their share was 88.4% with performance of 141.8%.

- Race/Ethnic – White, not Hispanic (79.3%) down from 84.7%. This group accounts for the vast majority of spending in every segment but lost share in Vet $ again in 2024. Their 120.0% performance is also down from 127.6% and they fell from #4 to #7 in importance in Veterinary Spending. All spent more, but the Minority increase was +56.4%, while Whites were up +8.4%. This caused the drops in share and performance.

- Area – Urban Areas (78.9%) down from 79.0% Suburban CU’s are the biggest spenders in every segment. All areas spent more and the lifts were in double digit % and very close in size. The Rural lift was slightly bigger. This explains why the drop in share was so small and caused their performance to stay at 97.6%. They’re still last in importance.

- Income – Over $100K (66.2%) up from 61.1% Their performance also grew from 167.7% to 174.5%. Higher income is still the most important factor in Veterinary spending. The only drops were $30>49K, -$0.27B and $70>149K, -$0.18B. The $150K> groups spent $5.68B more. This drove the big lifts in share and performance.

- # in CU – 2 or 3 People (62.5%) up from 61.9% This smaller group had a slight gain in share and their performance grew from 129.8% to 130.5%. CU Size’s rank in importance in Vet Spending moved up from #7 to #4. All but Singles, -$0.01B, spent more. 2/3 People CUs were +$3.69B, 66% of the overall lift in Vet Spending.

- Occupation – All Wage & Salaried (71.6%) up from 68.6% and their performance increased from 112.6% to 115.9%. In the group, all spent more. Outside the group, only Retirees, -$0.83B, spent less. White Collar workers spent $4.52B, +22.3% more. They drove the lifts in share in performance. Mgrs/Prof had the biggest lift, +$3.89B. We should also note that their perfomance lift was slowed a little because they had 1.9 million more CUs than in 2023.

- Education – College Grads (68.9%) up from 64.9%. Income generally increases with education. It is also important in understanding the need for regular Veterinary care. Their performance also increased from 135.8% to 143.2% and they stayed #2 in importance. Only <HS Grads & HS Grads w/some College spent less in 2023. College grads (48.1% of CUs) generated 94.6% of the 23>24 lift, which drove the increases in share and performance.

- CU Composition – Married Couples (63.8%) up from 61.5% Their performance also rose to 132.9% from 127.7% and they stayed #3 in importance. Only Married, +Adults, No kids, Single Parents & Singles spent less. The lifts in share and performance were due to All Married being +$4.39B, +20.0%.

- # Earners – 2+ CUs, 1 or 2 Earners (63.8%) up from 60.2% Their Performance also grew from 119.9% to 127.3%. # Earners moved up from #6 to #5 in importance. Only No Earner CUs of any size spent less. 2 Earners, +$4.61B, +29.4%, drove the group’s lifts in share and performance.

- Age – 35>64 (60.4%) down from 60.8% Their performance also slowed a little from 116.7% to 116.6% but they stayed 8th in importance. Only 55>64, -$0.34B & 65>74, -$0.09B spent less. The 54>64 drop along with a +$2.13B lift by <35 were the big factors in the Group’s minor drops in share and performance.

Spending disparity rose in 6 categories. The average group performance was 128.4%, up from 125.4% in 2023 so spending became less balanced. Notably, a smaller group size made CU Size & # Earners more important. However, the 3 most important groups, $100K> Income, College Degrees & Married Couples are the same as 2023.

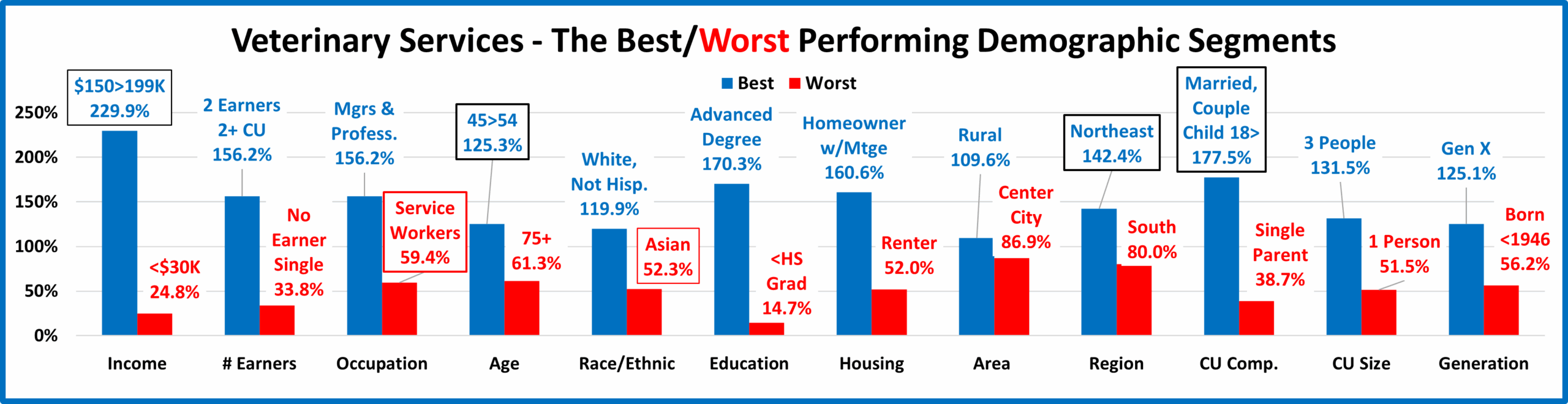

Now, we’ll look at 2024’s best and worst performing Veterinary spending segments in each category.

There are no surprising winners or losers but 6 are different from 2023, down from 9 last year. This is 3 more than Services, but 3 less than Supplies and 9 less than Food. Also, the average difference between Best & Worst was 99.4%, much more than 89.8% in 2023. There was considerable turmoil and 9 of 12 categories had increased disparity. The average difference grew considerably, so spending was less balanced. Changes from 2023 are “boxed”. We should note:

- Income– The Winner changed from $200K>. The gap is 205.0%, 30% more than 2023.

- Earners – No change in Winner or Loser, but the gap widened by 22.7%.

- Occupation – Service Workers replaced Blue Collar at the bottom but the gap only widened by +0.7%.

- Age – 45>54 replaced 55>64 yr-olds on top and the gap narrowed by -3.9%.

- Race/Ethnic; Asians replaced African Americans on the bottom. The gap narrowed a lot, -35.3%.

- Education; Housing; Area – These all had an expected repeat winner & loser and the performance gap increased for Education: +24.6%; Housing: +20.4%; Area: +1.3%.

- Region – Northeast replaced West at the top. The South has now finished last for 9 years in a row, but the win/lose gap increased by 9.1%. Also, just 2 regions performed at 100+%, down from 3 in 2023.

- CU Composition – Married, Child 18> replaced Couple Only on top. The gap widened, +42.7%.

- # in CU – No changes, but the gap grew by +5.7%. Only 1 & 5+ people CUs perform below 100%.

- Generation – No changes and the performance gap narrowed by -2.3%.

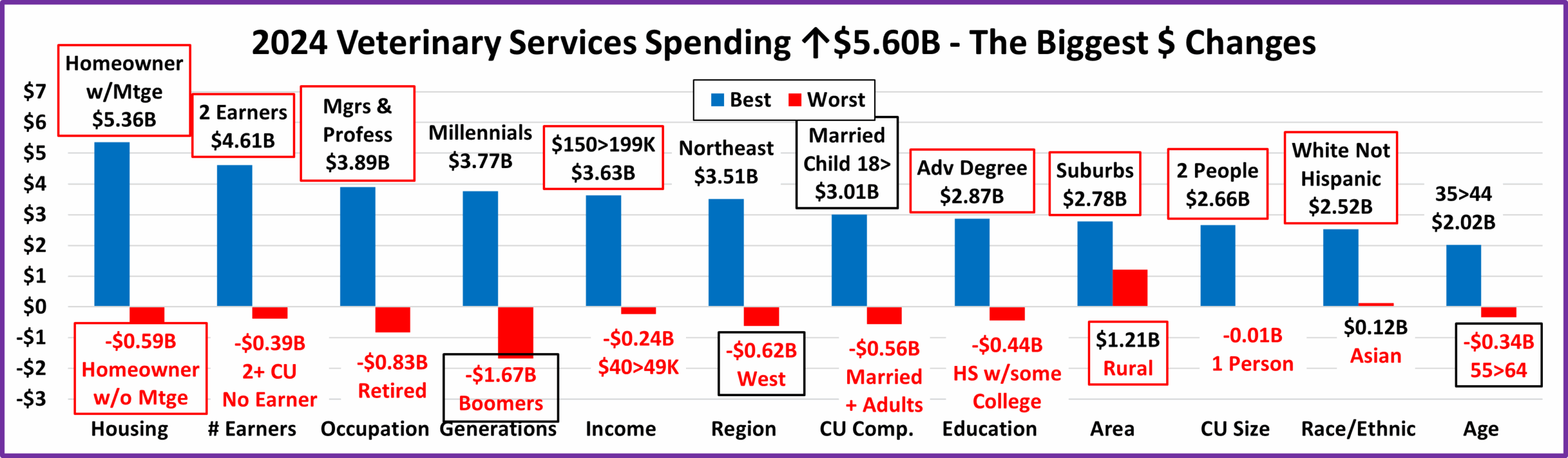

It’s time to “Show you the money”. Here are segments with the biggest $ changes in Veterinary Spending.

We saw some turmoil in performance. It lessens here. There were 10 repeats, and 4 segments flipped from 1st to last or vice versa. Last year there was 1 repeat and 13 flips. There were no truly surprising winners and there were only 2 somewhat surprising losers – Boomers & the West. In 2024 there were 2 categories in which all segments spent more. In 2023, there were 4. Plus, in 2023, 82.3% of 96 demographic segments spent more. In 2024, that slowed a little to 81.3%. If you consider 7.4% inflation, 69.8% still spent more in 2024.

- Housing – Homeowners w/Mtges stayed on top and those w/o Mtges stayed on the bottom.

- Winner – Homeowner w/Mtge – Veterinary: $24.46B; Up $5.36B (+28.0%) 2023: Homeowner w/Mtge

- Loser – Homeowner w/o Mtge – Veterinary$: $27B; Down $0.59B (-6.0%) 2023: Homeowner w/o Mtge

- Comment – In 2023, all segments spent more. In 2024, only Homeowners w/o Mtge spent less. Renters were +$0.84B, +12.5+. They account for 35.1% of CUs but only 18.3% of Veterinary spending, 52.0% performance. All Homeowners were +$4.77B, +16.5% and had 125.9% performance.

- # Earners – 2 Earners won again while No Earner, 2+ CUs replaced No Earner, Singles as the loser.

- Winner – 2 Earners – Veterinary Spending: $20.30B; Up $4.61B (+29.4%) 2023: 2 Earners

- Loser – No Earner, 2+ CU – Veterinary Spending: $3.03B; Down $0.39B (-11.3%) 2023: No Earner, Single

- Comment – Only No Earner CUs spent less. The 2nd largest lift was +$1.13B by 3+ Earner CUs. We should note that the increase by 1 Earner, Singles was only +$0.01B.

- Occupation – Mgrs/Prof won again but Retirees replaced Blue Collar on the bottom.

- Winner – Mgrs & Professionals – Vet Spending: $18.66B; Up $3.89B (+26.4%) 2023: Mgrs & Professionals

- Loser – Retired – Vet Spending: $6.08B; Down $0.83B (-12,0%) 2023: Blue Collar

- Comment – Only Retirees spent less. Amazingly, All Other, Unemployed had the 2nd biggest lift, +$0.79B. White Collar workers were +$4.52B, 80.7% of the Veterinary increase from 42.4% of CUs.

- Generation – Millennials are a new winner. Boomers flipped to the bottom.

- Winner – Millennials – Veterinary: $12.99B; Up $3.77B (+40.8%) 2023: Baby Boomers

- Loser – Baby Boomers – Veterinary: $10.27B; Down $1.67B (-14.0%) 2023: Born <1946

- Comments – Only Baby Boomers spent less. This comes after a +$2.21B lift in 2023. Millennials were more consistent. In 2023, they finished a close 2nd to the Boomers, +$2.09B. In 2024, they led the charge. Gen X is the most consistent. 23>24: +$2.34B; 22>23: +$1.13B; 21>22: +$0.46B (Note: Vet $ were -$2.95B in 2022.)

- Income – $150>199K stayed on top and $40>49K replaced <$30K at the bottom.

- Winner – $150>199K – Veterinary Spending: $8.98B; Up $3.63B (+67.9%) 2023: $150>199K

- Loser – $40>49K – Veterinary Spending: $1.52B; Down $0.24B (-13.4%) 2023: <$30K

- Comment – Only the $30>49K, $70>99K & $100>149K groups spent less. All big groups, under/over $70K & $100K had increases. The $150K> group drove the lift. They were +$5.68B (101% of the total Vet increase)

- Region – The West flipped to the bottom and the Northeast replaced them on top.

- Winner – Northeast – Veterinary Spending: $10.23B; Up $3.51B (+52.3%) 2023: West

- Loser – West – Veterinary Spending: $9.69B; Down $0.62B (-6.0%) 2023: Midwest

- Comment – All Regions but West spent more. The 2nd biggest lift was +$2.28B by the South.

- CU Composition – Married, Oldest Child 18> flipped to the top. Married, + Adults replaced them on the bottom.

- Winner – Married, Oldest Child 18> – Veterinary: $5.80B; Up $3.01B (+107.8%) 2023: Married, Couple Only

- Loser – Married, + Adults – Veterinary: $1.16B; Down $0.56B (-32.6%) 2023: Married, Child 18>

- Comment – Single Parents & Singles also spent less. 2023 favored CUs with no children. 2024 had no clear pattern. However, Married, With Children were +$3.78B, +41.6%. The largest % lift by any big group.

- Education – Adv. College degree stayed on top. HS w/some College replaced HS Grads at the bottom.

- Winner – Adv. College Degree – Veterinary Spending: $14.72B; Up $2.87B (+24.2%) 2023: Adv Degree

- Loser – HS Grads w/some College – Veterinary Spending: $5.11B; Down $0.44B (-8.0%) 2023: HS Grads

- Comment – In 2023, only <HS & HS Grads had spending decreases. In 2024, <HS & HS Grads w/some College spent less. Total <College was positive, +$0.30B. College Grads were +$5.30B, +22.9%. BA/BS finished a close 2nd to Adv. Degrees, +$2.43B, +21.5%.

- Area Type – Both Winner & Loser held their spots.

- Winner – Suburbs 2500> – Veterinary Spending: $19.99B; Up $2.78B (+16.2%) 2023: Suburbs 2500>

- Loser – Rural – Veterinary Spending: $8.69B; Up $1.21B (+16.1%) 2023: Rural

- Comment – In 2020 & 2021 all groups spent more. In 2022, all spent less. In 2023 & 2024, all spent more again. Since 2020, all segments have the same spending pattern. In 2024, Center City stayed in 2nd place, +$1.61B, +14.7%. The Suburbs 2500> have the biggest share of Vet $, 48.5% and generated 49.6% of the lift.

- # in CU – 2 People stayed on top and 1 Person replaced 4 People on the bottom.

- Winner – 2 People – Veterinary Spending: $17.79B; Up $2.66B (+17.6%) 2023: 2 People

- Loser – 1 Person – Veterinary Spending: $6.39B; Down $0.01B (-0.2%) 2023: 4 People

- Comment: In 2022, all spent less. In 2023, only 4 People CUs spent less. In 2024, it was 1 Person, -$0.01B. 2 People still had the biggest increase but the other lifts were more balanced. 3 people: +$1.03; 4 people: +$1.04B.

- Race/Ethnic – Whites stayed on top while Asians replaced African Americans at the bottom.

- Winner – White, Not Hispanic– Veterinary: $32.72B; Up $2.52B (+8.4%) 2023: White, Not Hispanic

- Loser – Asian – Veterinary: $1.11B; Up $0.12B (+12.7%) 2023: African Americans

- Comment– All groups spent more – more balance. Minorities were +$3.08B, 55% of the Vet lift. Only Asians had a minor lift. African Americans: +$1.86B, +164.0%; Hispanics: +$1.10B, +32.8%.

- Age – 55>64 flipped to the bottom. 35>44 replaced them on top. BTW: That’s the 3rd consecutive flip for 55>64.

- Winner – 35>44 yrs – Veterinary Spending: $8.52B; werUp $2.02B (+31.2%) 2023: 55>64 yrs

- Loser – 55>64 yrs – Veterinary Spending: $7.95B; Down $0.34B (-4.1%) 2023: 45>54 yrs

- Comment: All segments spent more in 23. In 24, 65>74 also spent less, -$0.09B. Spending skewed a little younger. <45: +$4.15B; 45>: +$1.45B. The 2nd biggest lift was +$1.67B by 25>34. #3 was +$1.53B by 45>54.

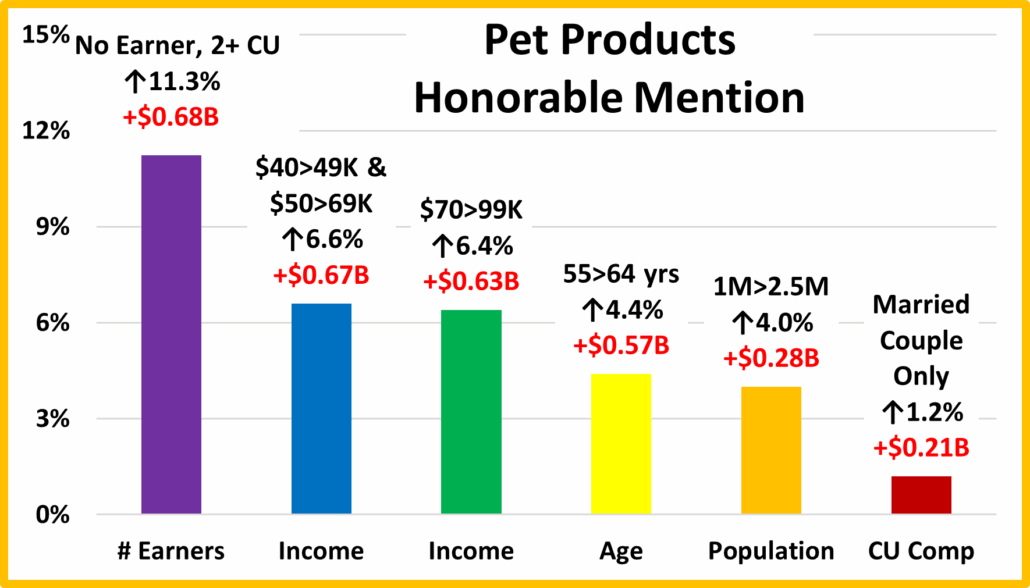

We’ve now seen the winners and losers in terms of increase/decrease in Veterinary Spending $ for 12 Demographic Categories. 2022 had a $2.95B drop. The decrease brought a lot of turmoil in the $ changes. In 2023 there was a huge turnaround as spending rose $5.95B, +20.0% and reached $35.66B. However, the turmoil in $ change continued. In 2024, the big lift continued, +$5.60B, +15.7% to $41.26B. Veterinary Services passed Pet Food and became #1 in spending by Pet Industry Segments. In 2024, in the change chart, 10 held their spot and only 4 flipped from 1st to last or vice versa. In 2023 there was 1 hold and 13 flips. In 2024, there was far less turmoil and greater stability. There were similarities between 2023 & 2024 but 2024 wasn’t always best. In 2023, 82.3% of demographics spent more and there were 4 categories where all segments had increases. In 2024, 81.3% spent more and there were 2 categories where all segments spent more. The “hidden gems” were still easy to find. Here are some segments that didn’t win but helped drive the big lift in Veterinary spending. These groups don’t win an award, but they certainly deserve…

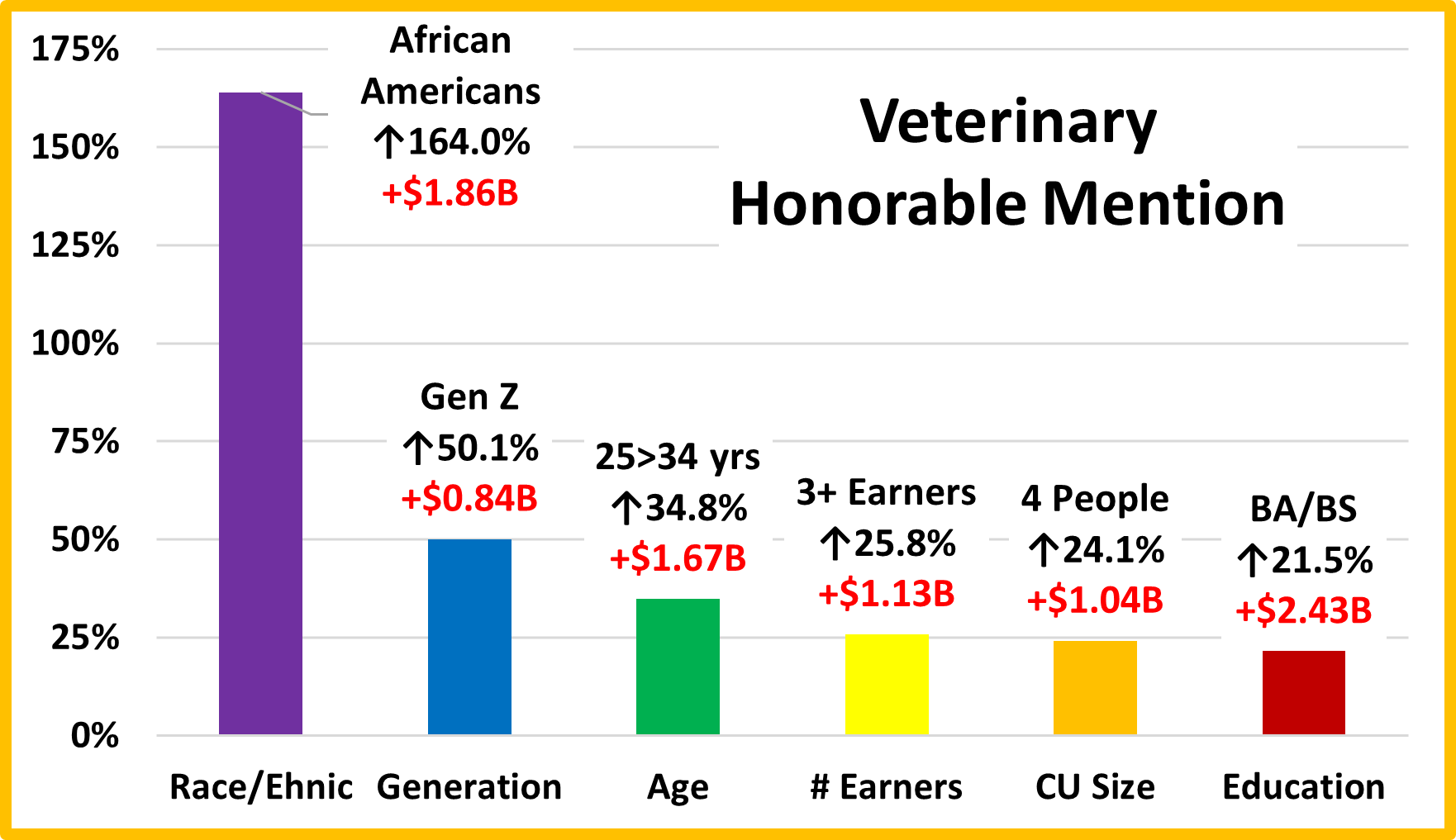

HONORABLE MENTION

The big lift by African Americans shows more racial balance & high income is not an absolute necessity. Gen Z continues to increase their commitment to Pet Parenting. Veterinary Services spending is skewing a little younger as the 25>34 yr-olds and Gen Z become more aware of its importance. Income matters most but the # earners is increasing in importance. 3+ earners have high income and increased their Vet $ by $1.1B. 2 & 3 People CUs spend the most but the key is 2+. 4 people CUs still earn their share of Veterinary spending with 105% performance. Higher Education usually means higher income which helps with growing Vet prices, but it is also important in understanding the need for a Vet. This group shows that the lift was widespread.

Summary

In 2020 the pandemic focused Pet Parents on the needed segments. This drove a $3B increase in Veterinary $. Boomers & Millennials led the way, but the lift was widespread as 85% of demographic segments spent more. In 2021 the lift grew to a record $7.82B with 93% of all segments spending more including 9 categories where all segments had increases. In 2022, the “binge” was not repeated. Inflation also increased radically to 8.8% and spending fell -$2.95B (-9.0%). Only 23% of demographics spent more and in 3 categories all segments decreased spending.

In 2023 Inflation grew to 9.4% but the higher income groups stepped up. The $30>49K segments also found the $. The result was a $5.95B, +20.0% increase as Veterinary Spending reached $35.66B. In 2024, Vet Spending was +$5.60B, +15.7% and reached $41.26B, now #1 in the Pet Industry. 81.3% of demographics spent more (down from 82.3%) and in 2 categories all segments increased spending (down from 4). Even considering the 7.4% inflation, 69.8% spent more.

The performance of big spending groups is very important in all industry segments. In Veterinary we identified 7 demographic categories with high performing (120+%) large groups, 2 more than 2023. It is also 1 more than Supplies & 2 more than Pet Food, but 1 less than Services. The big groups with a high-performance level in Veterinary are:

- Income: $100K> (174.5%) Performance increases with income but doesn’t reach 100+% until income reaches $100K

- Education: College Grads (143.2%) Performance increases with education, but only College Grads are 100+%.n

- CU Composition: Married Couples (132.9%) All Married CUs, but those with extra adults (no kids) perform at 100+%.

- CU Size: 2>3 People (130.5%) They are the top 2 performers, but only 5+ (93.8%) & 1 (51.5%) are <100%.

- # Earners: 2+ CUs, 1 or 2 Earners (127.3%) Only No Earner or 1 Earner CUs of any size perform <100%.

- Housing: Homeowners (125.9%) Only Homeowners w/Mtge (160.6%) perform above 100%.

- Race/Ethnic: White, Not Hispanic (120.0%). More Balanced, but Minorities still only perform between 52% and 68%.

Consumers have no control over Race/Ethnicity but can make decisions in the other categories. Income is still the most important factor. The others are important but lower in performance – 120>143%. Spending grew in 2024 and became less balanced, now with 7 big groups performing over 120% (up from 5). Another indication of this is that the average spending disparity between the best and worst performing segments grew from 89.8% to 99.4%. We should also note that the 50/50 spending dividing line increased from $124K to $141K, further emphasizing income’s importance.

Perhaps the biggest concern is high inflation. In 2021 spending grew 31.5% in the pandemic surge. Inflation was relatively high at 4.2% but 84% of the growth was real. In 2022 spending fell -9.0%. Inflation was 8.8% so the amount sold was really down -16.4%. In 2023, inflation reached a record 9.4%. Spending was +20.0% so the “real” increase was 9.7%. In 2024, inflation slowed to 7.4% but the lift also slowed to 15.7%. The “real” increase was 7.7%. If high inflation continues, it could have a major impact on Veterinary Spending. We’ll see.

Finally – The “Ultimate” Veterinary Services Spending CU consists of 3 people – a married couple with a child still at home. Their child is 18>. They are 45>54 yr-old Gen Xers. They are White, but not of Hispanic origin. Both work. At least one of them has an Adv. College Degree and is a Mgr/Professional. Their total income is $150>199K. They live in a rural area in the Northeast and are still paying off the mortgage on their home.